What Is a SIMERP and How Does It Work? A Plain-English Guide for Employers

If you have started researching strategies to reduce employer payroll taxes and come across the term SIMERP, you are not alone in asking what it actually means and whether it might apply to your business.

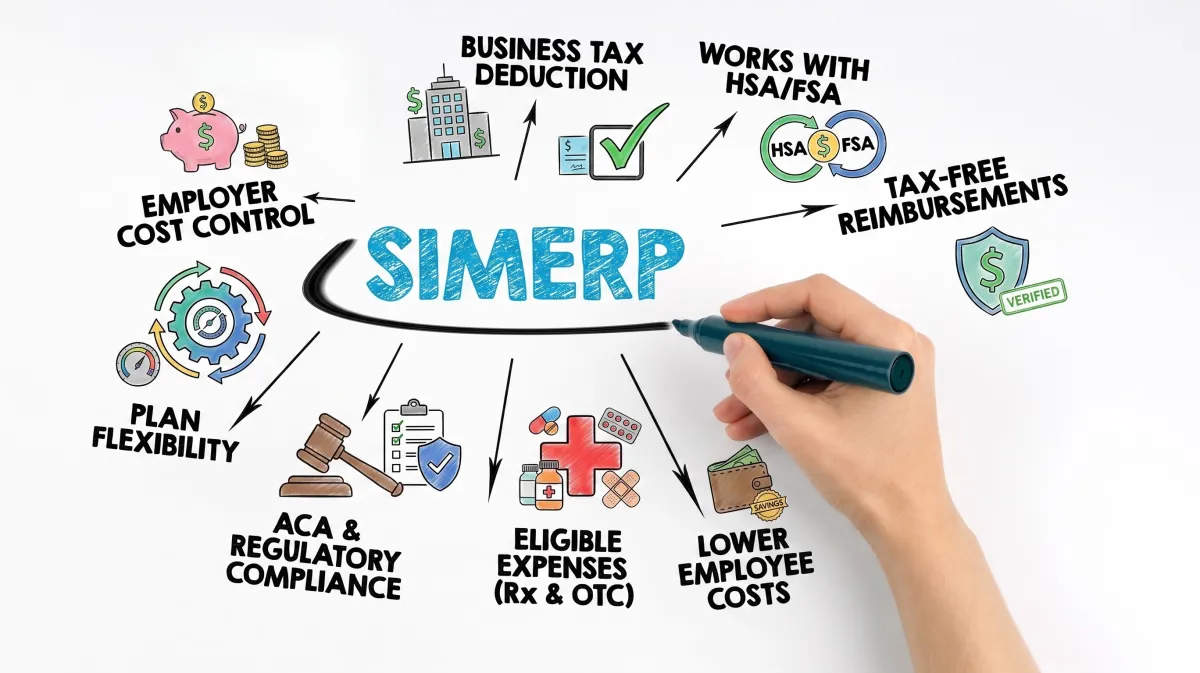

SIMERP stands for Self-Insured Medical Expense Reimbursement Plan. It is an employer-funded benefit plan established under IRS Code §105 that allows employers to reimburse employees for qualified medical expenses on a tax-free basis, while simultaneously reducing the employer's FICA payroll tax obligation. When structured correctly within a Section 125 cafeteria plan, a SIMERP can turn what would otherwise be taxable payroll into pre-tax benefit elections, creating meaningful and legally defensible savings for businesses with W-2 workforces.

If you are evaluating this for the first time, the employer payroll tax savings overview is a strong starting point for understanding the broader program before diving into the mechanics. This guide explains what a SIMERP is, how it works in practice, how it compares to other benefit plan types, and what employers typically need in place to evaluate fit.

The Problem Most Employers Don't Know They Have

Every pay period, employers remit 7.65% in FICA taxes on each employee's taxable wages covering Social Security and Medicare. For most businesses, this is treated as a fixed, non-negotiable line item. It gets processed automatically and rarely gets reviewed as something that could be structured differently.

But taxable payroll is not entirely fixed. It responds to how compensation and benefit elections are structured. When employees make qualifying elections on a pre-tax basis through an employer-sponsored plan, the amount of compensation subject to FICA decreases, and so does the employer's tax obligation.

Most businesses have never been introduced to the specific IRS mechanisms that make this possible. The SIMERP, operating within a Section 125 cafeteria plan structure, is one of those mechanisms, and it is one of the most underused tools available to employers who carry a substantial W-2 workforce.

What Exactly Is a SIMERP?

A SIMERP — Self-Insured Medical Expense Reimbursement Plan, is an employer-funded benefit plan authorized under IRS Code §105. Under this structure, the employer (rather than a traditional insurance carrier) funds reimbursements for employees' qualified medical expenses as defined under IRC §213(d). These reimbursements are processed on a tax-free basis through a certified Third-Party Administrator (TPA).

Unlike traditional group insurance plans, the employer in a SIMERP arrangement self-insures the benefit. The TPA handles the operational layer, including claims administration, plan documentation, payroll coordination, and compliance recordkeeping, so the employer does not carry that burden internally.

The critical tax advantage is created when the SIMERP is layered within a Section 125 cafeteria plan. When employees elect to participate through that structure, a qualifying amount of their compensation is reclassified from taxable wages into pre-tax plan elections, producing a lower taxable payroll base and lower FICA obligations for the employer.

Employers with questions about how the IRS code sections interact and what compliance infrastructure is required can review the full compliance overview, which covers ERISA, ACA, HIPAA alignment, audit protection, and plan documentation standards in detail.

How a SIMERP Works: Step by Step

Understanding the mechanics helps employers separate the structure from the marketing language around it. Here is how a compliant SIMERP operates in practice:

Step 1: The employer establishes the plan. A formal plan document is created under IRS §105 and §125, supported by a SOC 2 Type II certified Third-Party Administrator. The plan specifies qualified medical expenses eligible for reimbursement under §213(d), as well as participation rules and election mechanics.

Step 2: Eligible employees elect participation. W-2 employees who meet participation criteria opt into the plan through a Section 125 cafeteria plan election. This election is made on a pre-tax basis, which changes the payroll-tax treatment of the elected amount.

Step 3: Taxable payroll is reduced. Because the employee election is handled pre-tax, the taxable wage base subject to employer FICA is lower. A common example used in program modeling is $300 per month per employee, which can produce approximately $53.33 in monthly FICA savings per employee, or roughly $640 per year.

Step 4: The TPA administers reimbursements. As employees incur qualified medical expenses, claims are processed by the Third-Party Administrator. Records, elections, and plan documents are maintained in a format designed to support employer compliance and audit readiness.

Step 5: The employer captures the savings. The employer retains the payroll tax reduction generated by the lower taxable wage base. The program is structured to be self-funding, meaning implementation costs are typically covered by the FICA savings generated, with no upfront employer investment required.

Step 6: Existing health coverage remains in place. This is one of the most important distinctions: a SIMERP is designed to supplement current health insurance, not replace it. Employers keep their existing carriers, broker relationships, and plan designs exactly as they are. If you want to see how this plays out across specific workforce types, explore how the structure applies across industries, including modeled savings for automotive dealers, manufacturers, school districts, and healthcare organizations.

SIMERP vs. HSA, HRA, and FSA: What Is the Difference?

Employers evaluating this structure often ask how a SIMERP compares to other familiar benefit vehicles. It is a fair question; the acronym landscape in employer benefits is genuinely crowded. Here is a plain-English comparison:

FSA (Flexible Spending Account): Employee-funded via payroll deduction. Subject to annual contribution limits and use-it-or-lose-it rules. Does not generate a meaningful employer FICA reduction in the way a SIMERP does.

HSA (Health Savings Account): Requires enrollment in a qualifying High-Deductible Health Plan (HDHP). Has annual contribution limits. Employees own the account. Not usable for employers who want to keep existing non-HDHP coverage in place.

HRA (Health Reimbursement Arrangement): Employer-funded but tied to specific plan designs and often more restrictive in structure. Does not operate through the same Section 125 pre-tax election mechanics as a SIMERP.

SIMERP: Employer-funded through the overall plan structure. Does not require contribution limits tied to individual accounts. Designed to work alongside existing major medical coverage without forcing a plan replacement. Operates under §105 and §125, the specific combination that creates the FICA reduction benefit for employers.

For a structured side-by-side breakdown of how a SIMERP differs from FSAs, HRAs, and HSAs, along with compliance and due diligence answers that CFOs and HR leaders typically need before approving rollout, visit the full employer FAQ library.

Who May Be a Good Fit for a SIMERP?

Not every employer is positioned to benefit equally from this structure. Based on the program design, the strongest candidates typically share these characteristics:

100 or more W-2 employees: this is generally where the economics become meaningful enough to model, though final eligibility depends on workforce composition and payroll structure

Existing qualifying health coverage: employees must have compliant major medical coverage in place to participate, which supports ACA alignment

A stable W-2 workforce: industries with large hourly or support-staff populations, such as healthcare, manufacturing, automotive dealerships, and school districts, tend to see the most favorable savings profiles

Leadership looking to control payroll costs without disrupting benefits: the SIMERP adds a layer of value rather than requiring employers to restructure what is already working

Employers in labor-intensive industries can see composite savings models and industry-specific context by reviewing how the program fits different workforce types.

Key Benefits Employers Should Understand

When properly structured and administered, a SIMERP may offer the following advantages for qualifying employers:

Reduced FICA liability. Employers may save approximately $640–$1,120 per W-2 employee annually in payroll taxes, depending on participation and payroll structure.

Improved employee take-home pay. Participating employees may see an increase of approximately $150 per pay period through improved pre-tax payroll treatment, without any change to base compensation.

No disruption to existing benefits. Current carriers, broker relationships, and health plans remain intact. The SIMERP supplements rather than replace what is already in place.

Self-funding implementation. The program is structured so that FICA savings generated cover implementation costs; no upfront employer investment is required.

Full compliance infrastructure. Plan documents, employee elections, actuarial records, and audit-response materials are maintained by the TPA, so employers are not left building their own paper trail.

Common Mistakes When Evaluating a SIMERP

Employers who look into this structure sometimes make avoidable errors in their evaluation:

Treating it as a gray-area workaround. A SIMERP built on IRS §105 and §125 is not a novel or experimental strategy. It is grounded in a well-established employer benefit code, the same code sections that have supported cafeteria plans for decades. The structure is distinguishable from aggressive tax positions precisely because it depends on statute, not ambiguity.

Assuming it requires replacing the current health insurance. A properly designed SIMERP sits alongside existing coverage; it does not replace carriers, disrupt plan design, or require employees to change providers.

Waiting until year-end to evaluate. Every payroll cycle without an optimized structure is a cycle where potential FICA savings are not being captured. The cost of delay is real and measurable.

Not verifying TPA credentials. The quality of the Third-Party Administrator matters significantly. Employers should look for SOC 2 Type II certification, HIPAA-aware data handling, documented audit history, and ERISA-aligned plan support before moving forward with any SIMERP program.

Additional employer education on structuring and evaluating these programs is available through the Section 125 employer guides and resources.

Conclusion

A SIMERP is not a fringe concept or a tax shortcut. It is a formally structured, IRS-code-based employer benefit plan that, when implemented correctly within a Section 125 cafeteria plan, may allow qualifying businesses to reduce their FICA payroll tax exposure, without changing their existing health coverage, without cutting employee benefits, and without adding meaningful administrative burden to HR.

For businesses with 100 or more W-2 employees looking for a legal, documented, and sustainable way to reduce payroll tax costs, a SIMERP is one of the most viable structures available, and one that the majority of employers have never been introduced to in a serious planning conversation.

The first step is understanding whether your workforce profile and payroll structure may make it a fit. The employer payroll tax savings overview provides the full program context, and the live savings calculator lets you model potential annual savings by W-2 headcount before committing to anything.

Ready to Find Out If a SIMERP May Work for Your Business?

Get your free savings estimate today. Use the live calculator at Payroll Tax Optimization to model your potential FICA reduction based on your W-2 employee count, then request your free savings report for the full breakdown. No upfront cost, no obligation, and no need to replace your current health plan.